Regression Analysis: Currency Analysis with Sklearn Linear Regression

In this notebook, you will build a SKLearn linear regression model to predict Yen futures (“settle”) returns with lagged CAD/JPY exchange rate returns.

import numpy as np

import pandas as pd

from pathlib import Path

%matplotlib inline

# Currency pair exchange rates for CAD/JPY

cad_jpy_df = pd.read_csv(

Path("cad_jpy.csv"), index_col="Date", infer_datetime_format=True, parse_dates=True

)

cad_jpy_df.head()

| Price | Open | High | Low | |

|---|---|---|---|---|

| Date | ||||

| 1982-01-05 | 184.65 | 184.65 | 184.65 | 184.65 |

| 1982-01-06 | 185.06 | 185.06 | 185.06 | 185.06 |

| 1982-01-07 | 186.88 | 186.88 | 186.88 | 186.88 |

| 1982-01-08 | 186.58 | 186.58 | 186.58 | 186.58 |

| 1982-01-11 | 187.64 | 187.64 | 187.64 | 187.64 |

# Trim the dataset to begin on January 1st, 1990

cad_jpy_df = cad_jpy_df.loc["1990-01-01":, :]

cad_jpy_df.head()

| Price | Open | High | Low | |

|---|---|---|---|---|

| Date | ||||

| 1990-01-02 | 126.37 | 126.31 | 126.37 | 126.31 |

| 1990-01-03 | 125.30 | 125.24 | 125.30 | 125.24 |

| 1990-01-04 | 123.46 | 123.41 | 123.46 | 123.41 |

| 1990-01-05 | 124.54 | 124.48 | 124.54 | 124.48 |

| 1990-01-08 | 124.27 | 124.21 | 124.27 | 124.21 |

Data Preparation

Returns

# Create a series using "Price" percentage returns, drop any nan"s, and check the results:

# (Make sure to multiply the pct_change() results by 100)

# In this case, you may have to replace inf, -inf values with np.nan"s

cad_jpy_df["Return"] = cad_jpy_df[["Price"]].pct_change() * 100

cad_jpy_df = cad_jpy_df.replace(-np.inf, np.nan).dropna()

cad_jpy_df.tail()

| Price | Open | High | Low | Return | |

|---|---|---|---|---|---|

| Date | |||||

| 2020-05-29 | 78.29 | 78.21 | 78.41 | 77.75 | 0.076697 |

| 2020-06-01 | 79.27 | 78.21 | 79.36 | 78.04 | 1.251756 |

| 2020-06-02 | 80.40 | 79.26 | 80.56 | 79.15 | 1.425508 |

| 2020-06-03 | 80.70 | 80.40 | 80.82 | 79.96 | 0.373134 |

| 2020-06-04 | 80.71 | 80.80 | 80.89 | 80.51 | 0.012392 |

Lagged Returns

# Create a lagged return using the shift function

cad_jpy_df['Lagged_Return'] = cad_jpy_df.Return.shift()

cad_jpy_df =cad_jpy_df.dropna()

cad_jpy_df.tail()

| Price | Open | High | Low | Return | Lagged_Return | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2020-05-29 | 78.29 | 78.21 | 78.41 | 77.75 | 0.076697 | -0.114913 |

| 2020-06-01 | 79.27 | 78.21 | 79.36 | 78.04 | 1.251756 | 0.076697 |

| 2020-06-02 | 80.40 | 79.26 | 80.56 | 79.15 | 1.425508 | 1.251756 |

| 2020-06-03 | 80.70 | 80.40 | 80.82 | 79.96 | 0.373134 | 1.425508 |

| 2020-06-04 | 80.71 | 80.80 | 80.89 | 80.51 | 0.012392 | 0.373134 |

Train Test Split

# Create a train/test split for the data using 2018-2019 for testing and the rest for training

train = cad_jpy_df[:'2017']

test = cad_jpy_df['2018':]

# Create four dataframes:

# X_train (training set using just the independent variables), X_test (test set of of just the independent variables)

# Y_train (training set using just the "y" variable, i.e., "Futures Return"), Y_test (test set of just the "y" variable):

X_train = train["Lagged_Return"].to_frame()

X_test = test["Lagged_Return"].to_frame()

y_train = train["Return"]

y_test = test["Return"]

# Preview the X_train data

X_train.head()

| Lagged_Return | |

|---|---|

| Date | |

| 1990-01-04 | -0.846720 |

| 1990-01-05 | -1.468476 |

| 1990-01-08 | 0.874777 |

| 1990-01-09 | -0.216798 |

| 1990-01-10 | 0.667901 |

Linear Regression Model

# Create a Linear Regression model and fit it to the training data

from sklearn.linear_model import LinearRegression

# Fit a SKLearn linear regression using just the training set (X_train, Y_train):

model = LinearRegression()

model.fit(X_train, y_train)

LinearRegression()

Make predictions using the Testing Data

Note: We want to evaluate the model using data that it has never seen before, in this case: X_test.

# Make a prediction of "y" values using just the test dataset

predictions = model.predict(X_test)

# Assemble actual y data (Y_test) with predicted y data (from just above) into two columns in a dataframe:

Results = y_test.to_frame()

Results["Predicted Return"] = predictions

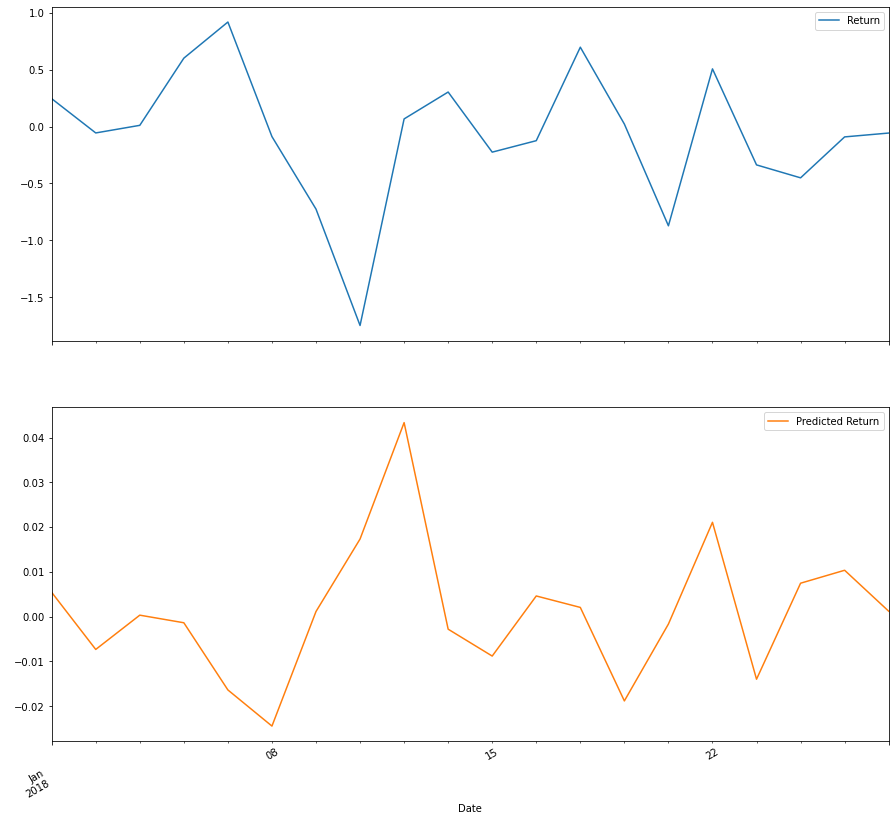

Results.head(5)

| Return | Predicted Return | |

|---|---|---|

| Date | ||

| 2018-01-01 | 0.245591 | 0.005434 |

| 2018-01-02 | -0.055679 | -0.007317 |

| 2018-01-03 | 0.011142 | 0.000340 |

| 2018-01-04 | 0.601604 | -0.001358 |

| 2018-01-05 | 0.919158 | -0.016366 |

# Plot the first 20 predictions vs the true values

# The trends lines should be similar

Results[:20].plot(subplots=True, figsize=(15,15))

array([<AxesSubplot:xlabel='Date'>, <AxesSubplot:xlabel='Date'>],

dtype=object)

Out-of-Sample Performance

Evaluate the model using “out-of-sample” data (X_test and y_test)

from sklearn.metrics import mean_squared_error

# Calculate the mean_squared_error (MSE) on actual versus predicted test "y"

# (Hint: use the dataframe from above)

mse = mean_squared_error(

Results["Return"],

Results["Predicted Return"]

)

# Using that mean-squared-error, calculate the root-mean-squared error (RMSE):

rmse = np.sqrt(mse)

print(f"Out-of-Sample Root Mean Squared Error (RMSE): {rmse}")

Out-of-Sample Root Mean Squared Error (RMSE): 0.6445805658569028

In-Sample Performance

Evaluate the model using in-sample data (X_train and y_train)

# Construct a dataframe using just the "y" training data:

in_sample_results = y_train.to_frame()

# Add a column of "in-sample" predictions to that dataframe:

in_sample_results["In-sample Predictions"] = model.predict(X_train)

# Calculate in-sample mean_squared_error (for comparison to out-of-sample)

in_sample_mse = mean_squared_error(

in_sample_results["Return"],

in_sample_results["In-sample Predictions"]

)

# Calculate in-sample root mean_squared_error (for comparison to out-of-sample)

in_sample_rmse = np.sqrt(in_sample_mse)

print(f"In-sample Root Mean Squared Error (RMSE): {in_sample_rmse}")

In-sample Root Mean Squared Error (RMSE): 0.841994632894117

Conclusions

Question: Does this model perform better or worse on out-of-sample data as compared to in-sample data?

Answer: With a lower RMSE, we have a better model. So with that in mind, we can conclude that the out-of-sample performance is better than our in-sample performance. The In-Sample performance RMSE is close to 1, whereas the RMSE for the out-of-sample is closer to 0.5. Thus, this model performs better on the out-of-sample performance.